After reading "

Web search queries can predict stock market volumes" I decided to replicate the study using

Google Insights for Search to look for more meaningful trends. A more in-depth post will be done later, here I am just presenting some cautious considerations for the readers of the study.

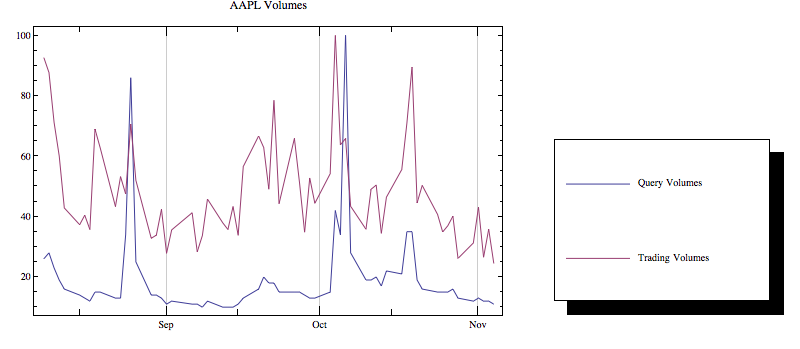

Part of the curious methodology of the paper was its filtering of non-working days. Using "AAPL" as an example, we can see why. How would the inclusion of the increased weekend queries influence the tests for granger causality?

|

| Normalized data of daily trading and query volumes for AAPL excluding weekends for last 90 days |

|

| Normalized data of daily trading and query volumes for AAPL with weekends for last 90 days |

No comments:

Post a Comment